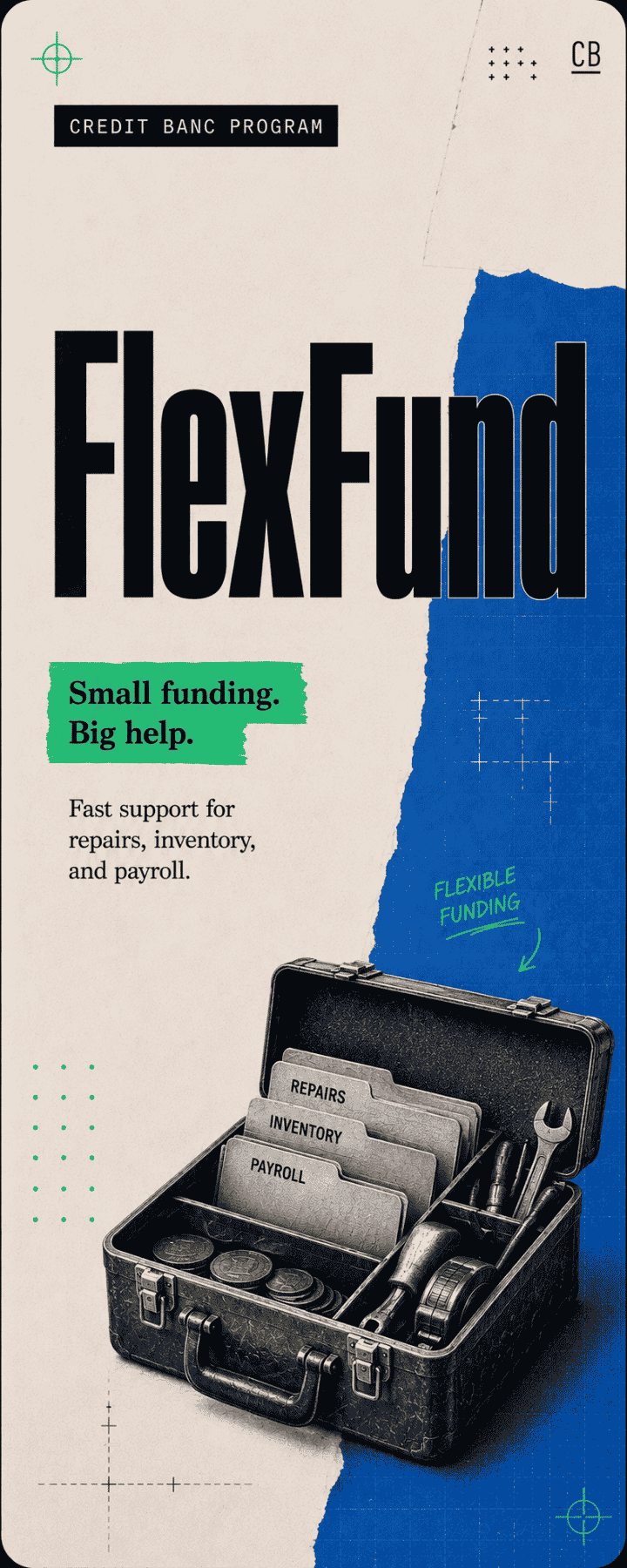

FlexFund Program

Good things come in small (funding) packages.

FlexFund is built for business owners who need a practical amount of capital without turning the whole process into a three-act drama. Use it for equipment, repairs, marketing, hiring, inventory, cash flow gaps, or a smaller business move that still needs to get done.

The point is simple: get useful capital in the door, keep the payment manageable, and avoid borrowing more than the situation actually calls for.

- Loan amounts from $15,000 to $50,000

- Funding in 10 days or less

- Terms up to 10 years

- Monthly payments

- Minimum FICO of 640

Best for

Business owners with a specific need that is too important to ignore, but not big enough for a massive financing package. FlexFund is a fit when the business needs a clean, manageable way to handle the next move without overborrowing or settling for short-term money with an attitude problem.